Optimum Communications ($OPTU) - SHORT thesis

This is not a takeover bid (Tender Offer) it’s new debt at +13%, which overpays the shares at $2.50, while Drahi sits in the protected bracket (Preferred) + MOIC (1.50x)

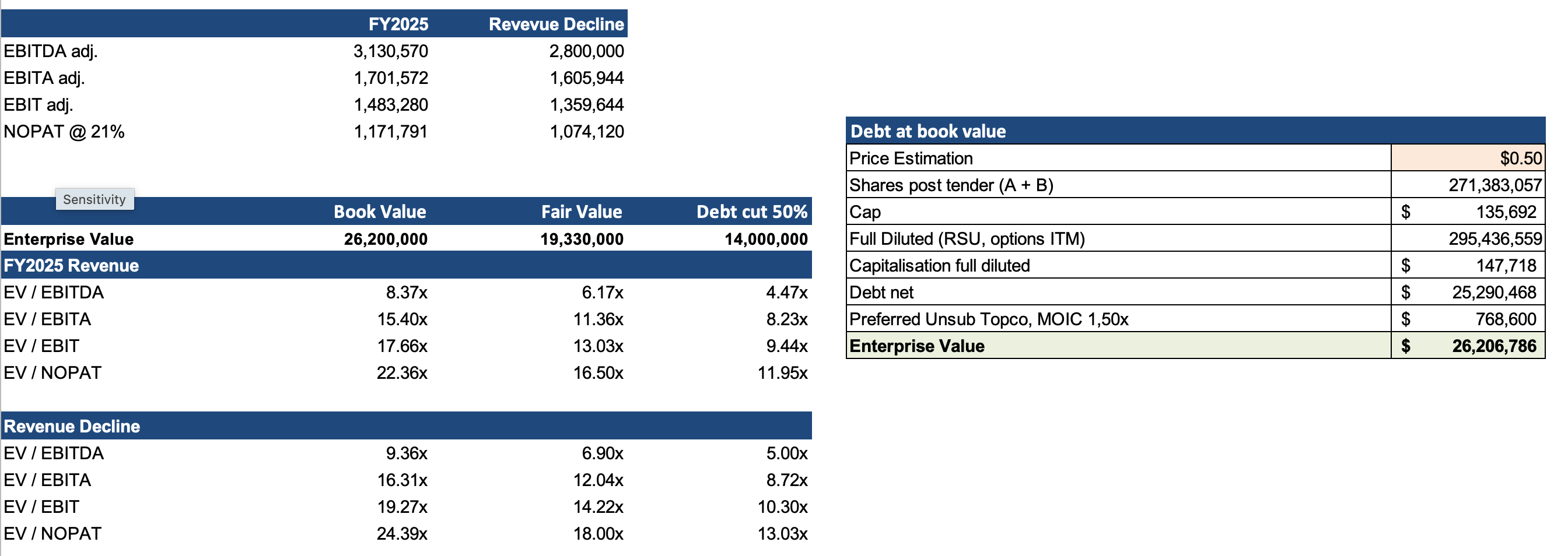

The Drahi cash tender offer at $2.50 is a temporary technical floor that artificially keeps the stub above its fundamental value until June 30. Once this bid disappears, the stock is expected to go down with more than $25 billion in net debt (+Senior Preferred), for an EBITDA declining to ~$2.8 billion and an EV of ~$26 billion dominated by debt (leverage x8). If we use comparables to calculate a mean multiple, for example Charter, there is nothing left for the common share: the stub should go below $0.50 and tend towards zero.

Performance of the shorts +55% (ROI)

The Situation

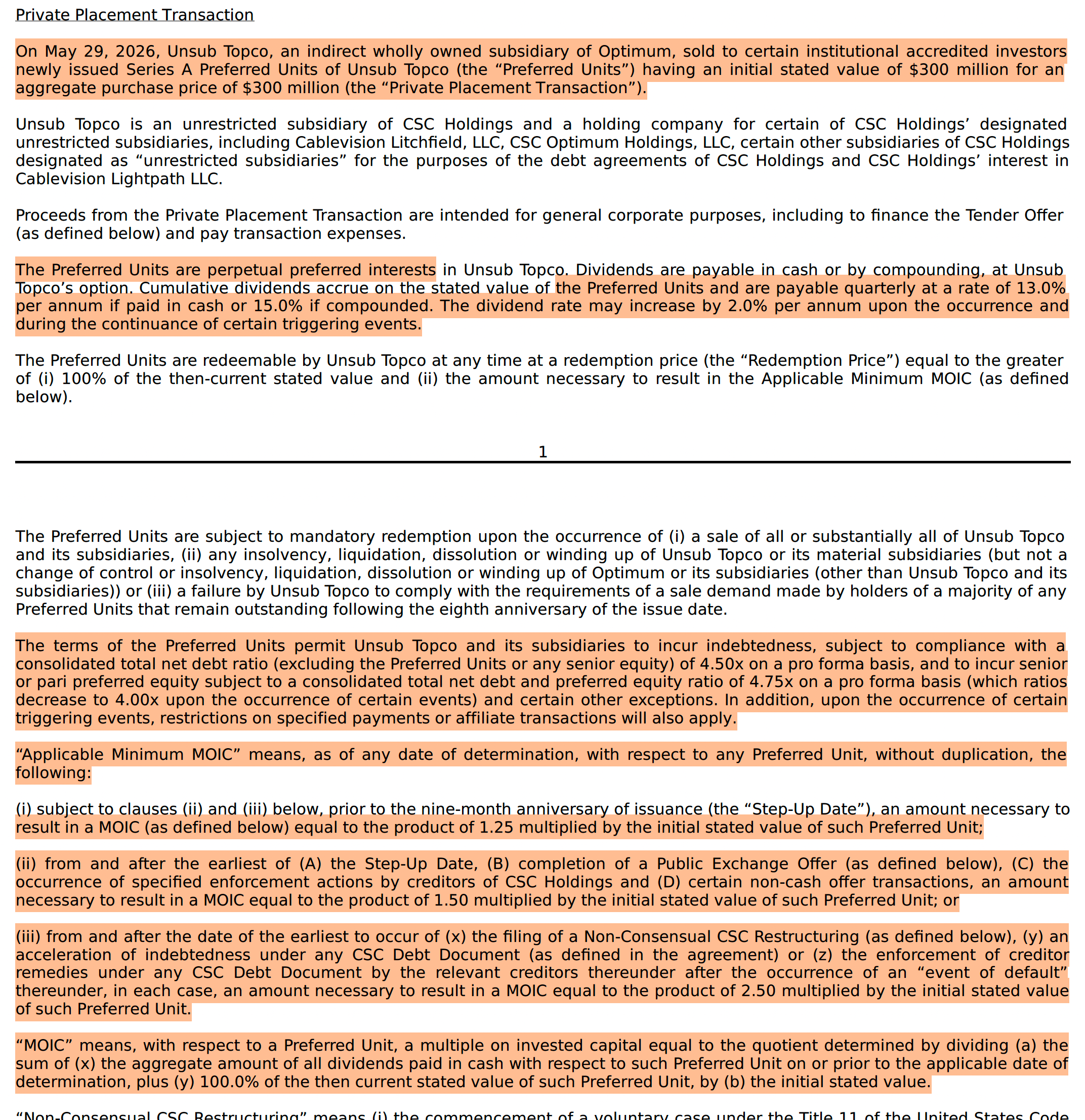

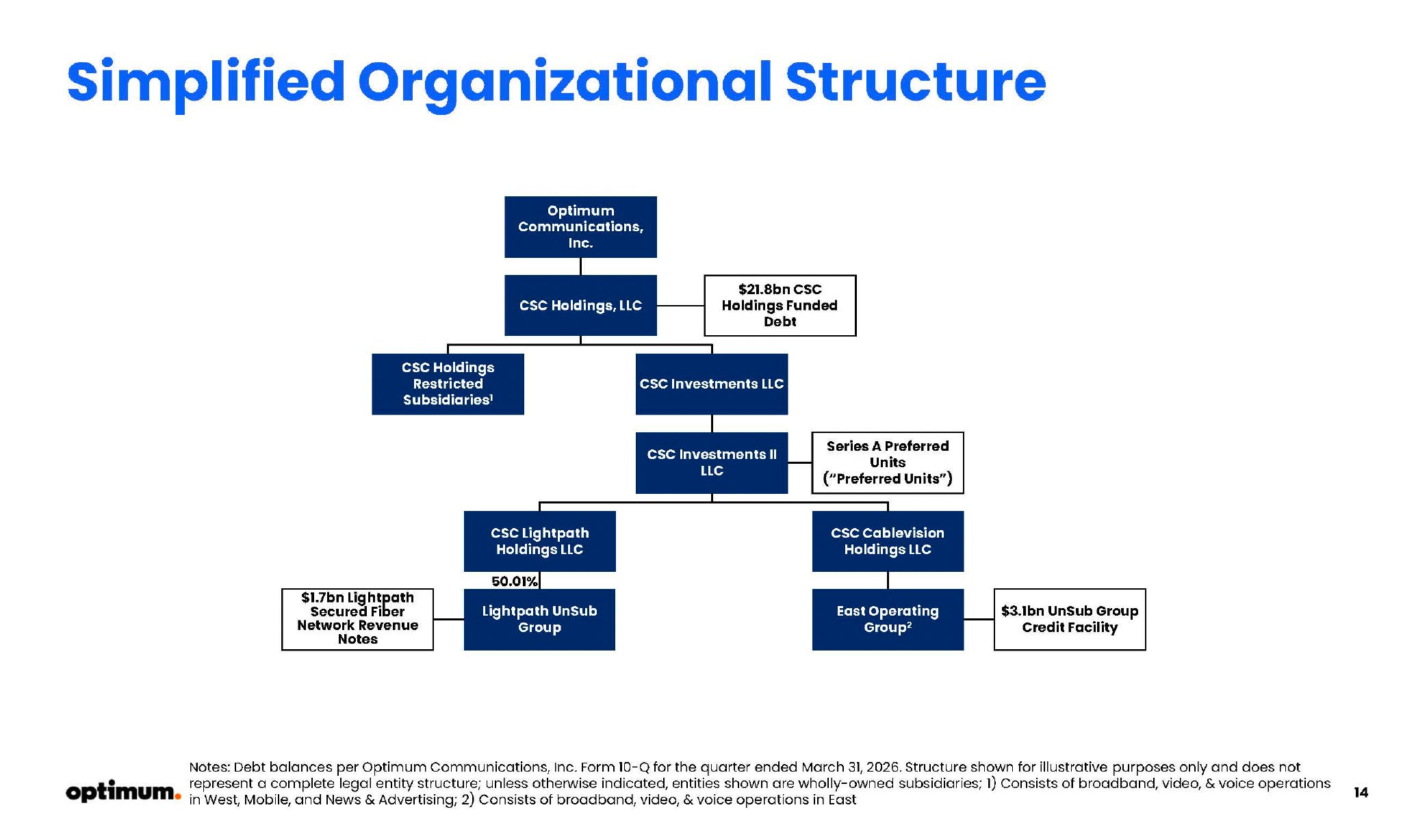

On May 29, 2026, Optimum placed its best assets, Optimum East Cable + 50.01% of Lightpath (the fiber) in an unrestricted subsidiary (Unsub Topco / CSC Investments II), out of reach of CSC Holdings creditors. It raised $512 million in senior preferences (including $300 million in cash) and, through this subsidiary, is launching a $2.50 tender offer on 120 million A shares ($300 million), financed by the preferential (13% + 2% debt).

The operation buyback shares that are more expensive than their true value with debt (Preferred share), which will cost more than 13% interest (option +2%). And add to that a MOIC of 1.50x ($750mm) or, in the worst-case scenario, 2.50x ($1.3Md).

The market treats the security as a takeover target (~$1.10) even though it is a liability management maneuver: Drahi buys out the free float before restructuring +$21 billion of CSC debt. The arbitration on the bid at $2.50 masks the fact that the balance sheet revealed in the 2026-Q1 and (8K results of June 1st) results leaves equity deeply underwater.

The key point: EV is anchored by debt. The total consolidated debt is $25 billion (book value), or about $19 million in fair value. The debt is already being processed at less than even (the market credits $0.77), which signals a distress that has already been priced. Ordinary shares (A + B) represent only a very small percentage of the EV. Whether the stub is rated $2.50, $0.65, or $0.30 changes almost nothing in the EV. So we must reason by the multiple, and the multiple imposes the value of the action.

Even if the stub is already placed at the $0.50 target, the multiples are untenable. At $0.50 + debt + pref. to MOIC 1.5x → EV +$26Md or by marking the debt at its fair market value → EV +$19Md. These two anchors are compared to EBITDA and post-D&A / post-tax measures.

Even at $0.50, it’s already too expensive. At par debt, we price 8-9x EBITDA, above Charter (~5.6x, the median sectoral telecom/cable ~6.0x). OPTU is in decline with an 8x leverage and, as it is being pre-restructured, deserves a discount, not a bonus.

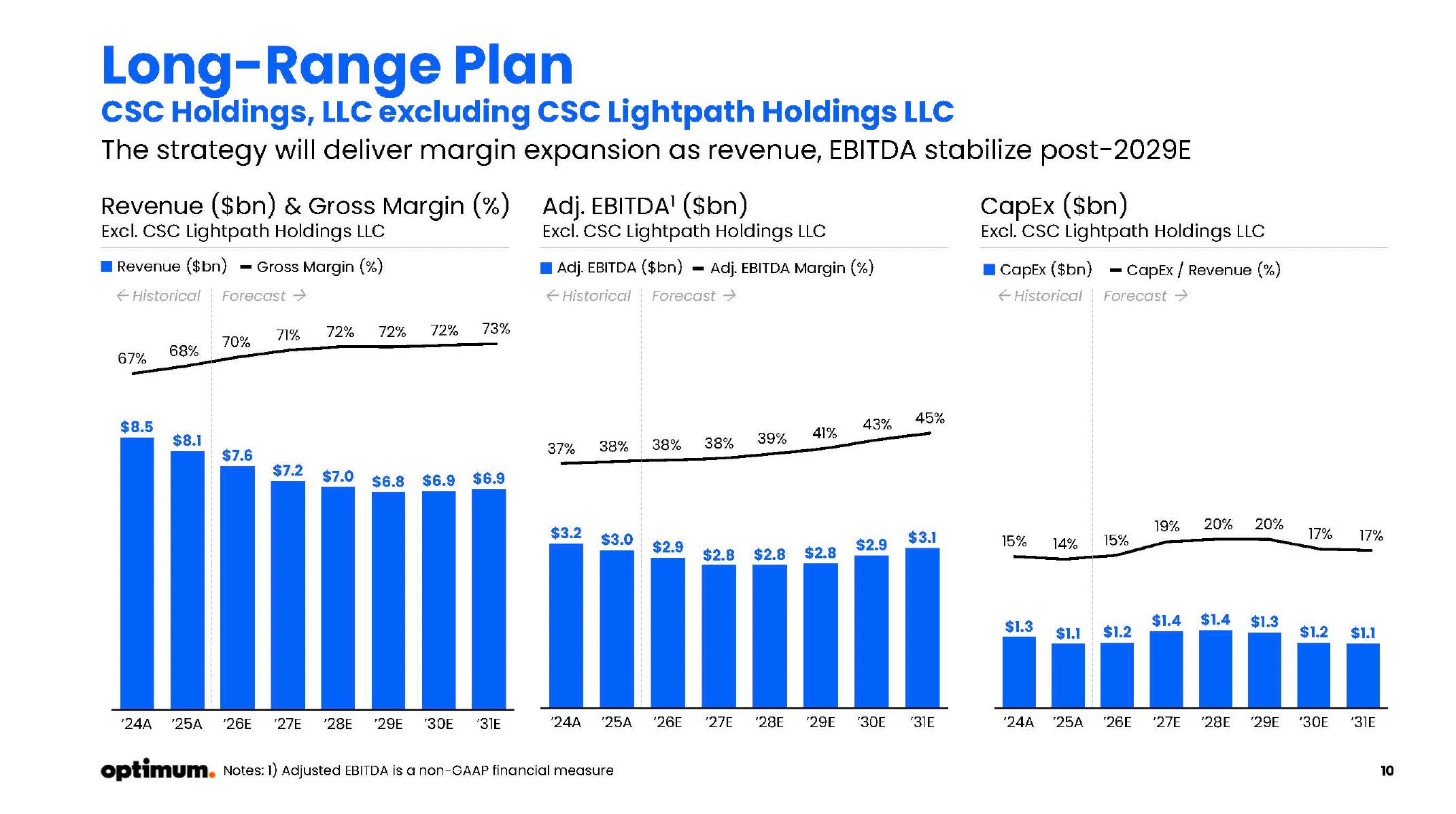

The cable is ultra-capitalistic the further one descends toward the actual economic result (post-D&A, post-tax), the more the multiple explodes up to 16x–24x NOPAT. It’s an absurd multiple for a company whose plan projects declining revenue ($8.5Md 2024A → ~6.8Md 2029E).

At a fair multiple of 5.5x–6.0x on central EBITDA (~2.8Md$), the enterprise is worth 17–19Md$. However, the debt is owed at par, and the Preferred one comes before the common one; this would give us $0 in the worst-case scenario, which seems realistic.

The market has already said so. Its fair value of the debt implies an EV of ~$19 billion, that is, ~$6 billion below the single par value debt ($25 billion). The creditors themselves price a haircut of ~6 billion dollars, and the equity is behind them in the queue. There is nothing left to convert into a value for the common.

If Drahi manages to clear +50% of the debt for nothing or equity, we arrive at a multiple of 5x EV/EBITDA and 13x EV/NOPAT. This would be the only scenario where a price of $1.20 per share would be justifiable. That is our Bear case for our short thesis.

Base Case: -0.50 $

Bull Case : 0.15 $–0.30 $ (pure option value) as the bid evaporates.

ROI +55%

Some notes

Drahi has rolled its shares into the senior preferred ($200mm), protected, with MOIC up to 2.5x if CSC goes into non-consensual restructuring. The best-informed insider stands out from the common for an instrument that wins if CSC collapses, here is indirect proof that the common is not worth much.

Legal precedent STG Logistics (Jan. 2026): In short, the STG Logistics judgment is a major blow to the financial tricks of over-leveraged companies. The judge ruled: a company does not have the right to use technical flaws in its contracts to transfer its best assets to a new subsidiary for the sole purpose of robbing certain creditors. From now on, the creditors set aside can directly sue the management and have these transfers frozen, which gives a formidable weapon to (Apollo, Ares, BlackRock) to block Drahi maneuvers.

Catalysers

I have identified several catalysts that will be favorable to the shorts, we don’t need them all to arrive, but a combination of two or three would be devastating.

Disappearance of the technical bid (June 30). As long as the Tender Offer is open, arbitragers keep the price close to $1.20. Upon expiration, the cash support evaporates and the stub resumes on its fundamentals.

A preliminary injunction freezing the drop-down would block Drahi ability to use Optimum East as collateral, and would push towards a non-consensual outcome thus toward the fiscal bomb and a disorderly Chapter 11.

CODI fiscal bomb ($4 billion). A restructuring triggering the deconsolidation of CSC creates a federal tax debt estimated at more than $4 billion, a joint and several liability at Optimum that directly destroys value for the listed entity.

Risk of delisting. Price under $1→ 30-day NYSE standard, notice of non-compliance (forced index/fund exits).

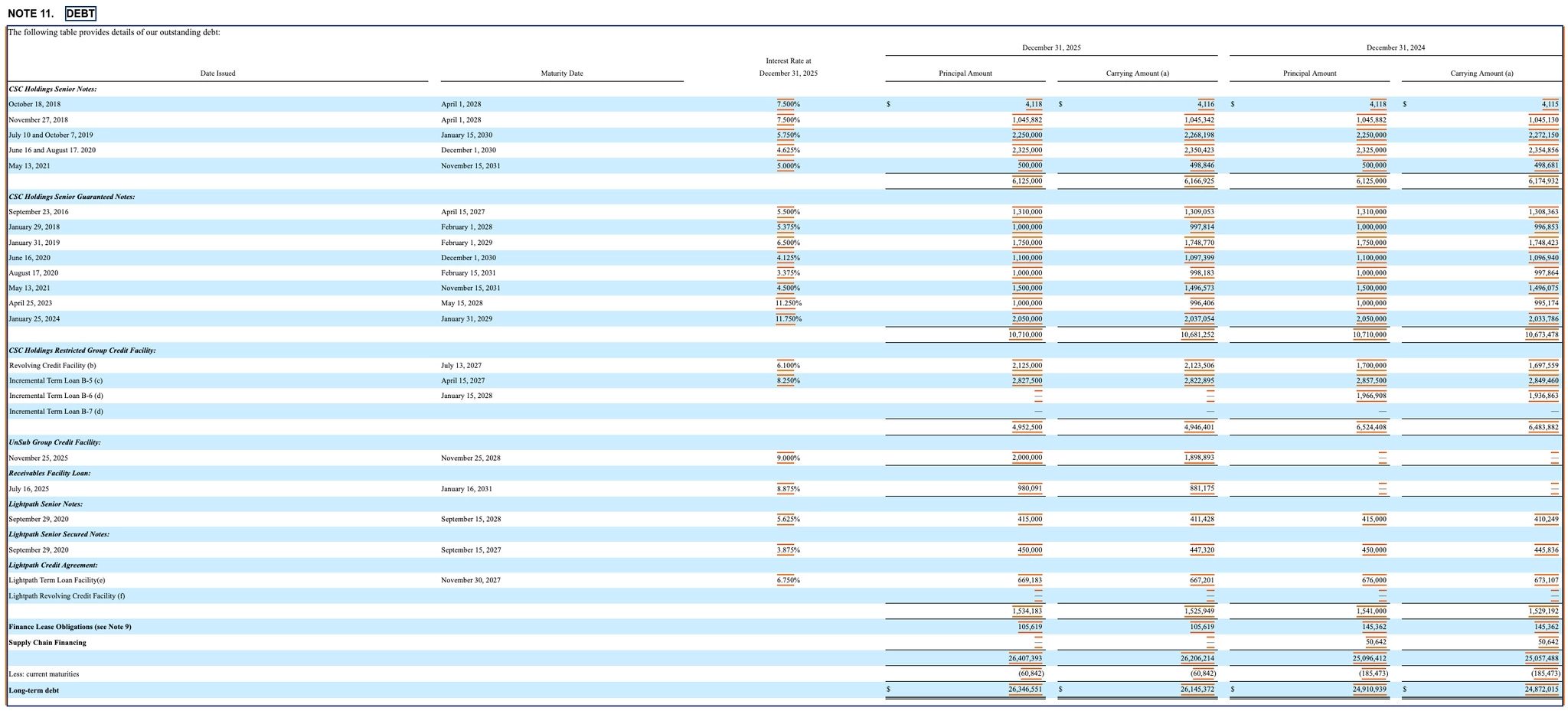

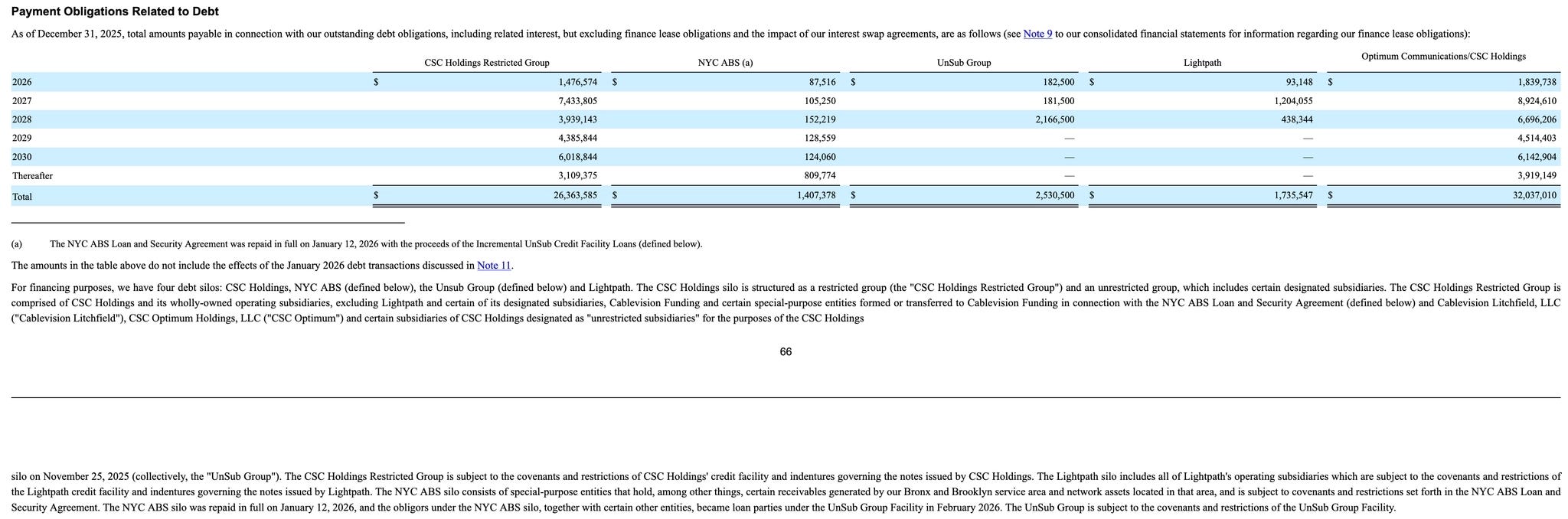

Maturity wall 2027 + cooperation agreement. Out of +21 billion dollars, ~6 billion dollars were due in 2027 (including $4.1 billion in April 2027). The Co-Op Agreement (June 2024) prohibits creditors from case-by-case deals → closes traditional LME and pushes toward a binary event.

Debt:

Their CAPEX cycle does not seem to be close to the end.

Their guidance seems very poor with an EBITDA declining for 2026-2027-2028.

I wanted to write a very short thesis that goes directly to the important points, but several things need to be analyzed and calculated. For example, the OPTU lawsuit against Apollo, Ares, BlackRock. His problems in Europe, Patrick Drahi is an investor who has made several leveraged acquisitions (LBO). He also seems very dishonest. I could have written a full paragraph about him that would give the shorts more arguments. Do your due diligence before doing anything else.

Again, my goal with this post is to have constructive comments or any argument that can destroy my thesis. I try to find the flaws in my thesis and learn more.

Max

Disclaimer: This newsletter is published for informational and educational purposes only. Nothing contained herein constitutes investment advice, a recommendation, or an offer or solicitation to purchase or sell any security or financial instrument. The author is not registered as an investment advisor, portfolio manager, or dealing representative with the Autorité des marchés financiers (AMF), the Ontario Securities Commission (OSC), the Securities and Exchange Commission (SEC), or any other securities regulatory authority in any jurisdiction. The author is an individual investor expressing personal opinions and sharing personal investment decisions. The author holds long and/or short positions in many of the securities discussed in this newsletter and may buy, sell, or modify these positions at any time without prior notice. The information presented is based on publicly available sources believed to be reliable, but no representation or warranty is made as to its accuracy, completeness, or timeliness. Past performance is not indicative of future results. Investing in micro-cap, small-cap, and special situations securities involves significant risks, including the potential loss of the entire investment. Readers should perform their own independent research and consult with a licensed financial professional before making any investment decisions.

I've been tracking this one and agree with your thoughts.

The tricky thing is sometimes lenders just give up value to the equity. And sometimes they give up way more than you would ever think is reasonable.

Recent examples are RGS, WW, NFE, BBGI. The lenders sometimes willingly take significant haircuts, but still allow the equity to survive in order to accelerate the restructuring process.

I think everyone realizes how insanely expensive the bankruptcy process has become, so the equity can use that as a source of bargaining leverage.

The MC would still be $250m at 50c, so maybe all this is not relevant in the OPTU case as that still implies a lot of value capture for the equity.

In your opinion, what are the chances of the tender falling through? Interestingly, you can buy 99 shares and tender the whole lot through the odd lot provision. Decent beer money.