Value in a Canadian office REIT at less than 5x AFFO

Intelligent change in capital allocation, several catalysts already underway, and massive buybacks. (TSX: TNT.UN) 🇨🇦

Disclaimer, I am a shareholder of True North Commercial Real Estate Investment Trust.

True North Commercial Real Estate Investment Trust (TSX: TNT.UN)

The REIT is an unincorporated, open-ended real estate investment trust established under the laws of the Province of Ontario. The REIT currently owns and operates a portfolio of 40 commercial properties consisting of approximately 4.6 million square feet in urban and select strategic secondary markets across Canada focusing on long term leases with government and credit rated tenants. The REIT is focused on growing its portfolio principally through acquisitions across Canada and such other jurisdictions where opportunities exist.

Introduction

True North Commercial has faced many challenges over the past 3 years. Losing large tenants, cutting their dividend by 50%, and then stopping it altogether. And the sale of several buildings they have not yet completed.

Since 2023, there have been several changes in the trust structure. The management in place seems competent, and we can see this with their decision to cut the dividend in difficult times.

The opportunity exists for many of the reasons mentioned above, and it's a good one for us.

It's rare to see a REIT company suspend its dividend and then proceed with share purchases. (It's a rare decision in this sector.) However, it is an intelligent capital allocation decision.

Based on volume over the last 3 months, we can estimate that they will be able to buyback around 11-12% next year (2025). This guarantees a good return, as well as a high margin of safety on the cost of buyback. It seems to me that they will have to start paying a dividend again in 2025 or 2026, because they will probably have a lot of money and will be taxed if they keep it for the second tax year.

Buyback

For non-Canadian residents or for those who don't know the difference between US and Canadian REITs. Crucial information for understanding why buyback are so advantageous on a Canadian and not an American REIT.

U.S. REITs are corporations while Canadian REITs are mutual fund trusts. U.S. REITs are required to pay out 90% of taxable income as shareholder distributions vs. a 100% rule for Canadian REITs. Canadian REITs tend to use more debt to finance operations, including mortgages secured by property holdings.

Macro

Here's an overview of Canada's rental office sector. Our focus is on the Alberta (Calgary) and Toronto markets. We are seeing a slowdown in construction and rental demand.

Insider

The Chairman and CEO own around 12%1 of outstanding shareholders. This also includes the “Special Voting Units” which give him a voting power of over 34%.

Risk

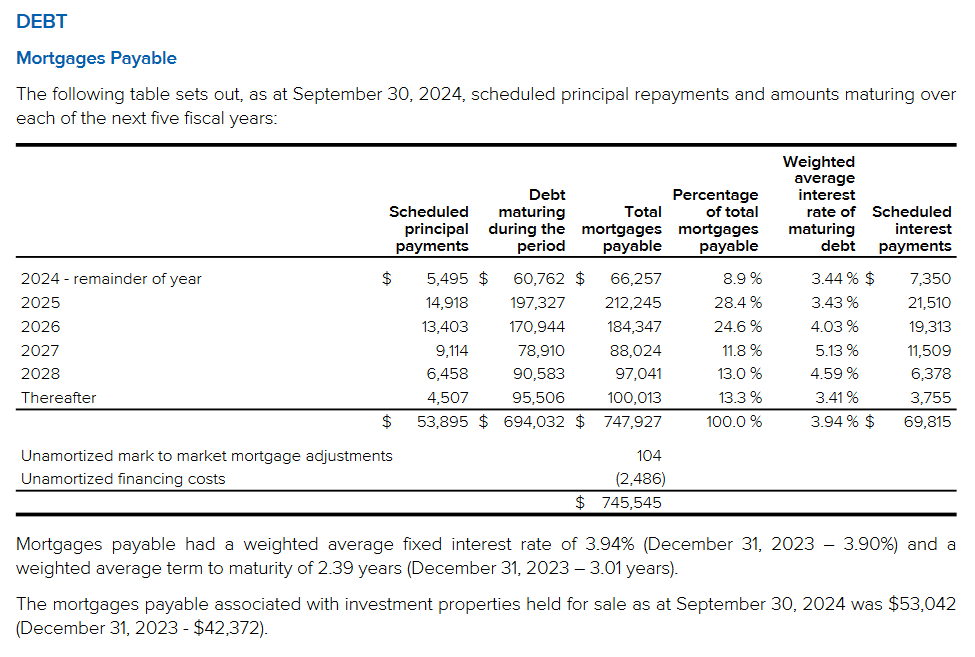

We have a few risks, such as losing other tenants. They're having trouble leasing their largest office in Calgary and Toronto. The burden of debt and mortgage renewal will be considerable in 2025-2026. And also not being able to sell the last buildings (3 left) for 2025.

Catalysts

We have a number of catalysts, some of which have already been activated.

Canada Rate drop (below of 3%)

Calgary & Toronto Office Recovery

More buyback at cheap value (14$ or less)

Introduction of a dividend by 2025 (A wave of buying by dividend investors is highly likely.)

Here are Canada 1, 5 and 10-year rates. What concerns us most is the 5- and 10-year rates. To estimate the current refinancing rate, we would need to add about +/- 1.20% to the 5-year rate.

Held for sale

Now we need to talk about the offices for sale, which will have a major impact on cash flow in 2024 and on the value in 2025.

Looking at the 2024 activities, we note that 4 offices were sold with their price.

This gives an idea of the average price for the Toronto and British Columbia region.

Here are 3 offices for sale, with a rough estimate of the value we could achieve.

It is estimated that the sale of the 3 offices will bring in around 70 million. Let's do a quick calculation. After fees paid and the remaining mortgage payment (I use 65%), we could get around 21 million.

With all that potential cash flow in 2025, there's a good chance of big buyback or a special dividend in 2025-2026. Nevertheless, it's likely to take several months to sell its big offices.

Value

If we remain conservative, with a price of 8x AFFO by the end of 2025, we can expect a price of between $16 and $20. If the dividend reaches a yield of 10% in 2026, there is likely to be a large number of buyers (investors/dividend hunters). We should be above $22.

I estimate that we should have an AFFO per share of between $2.30 and $2.60 with the remaining 37 offices. This would give us more than $2.10 in cash flow available for distribution by 2024-2025.

This gives us an IRR of around 30% for 2 years (25 months) if the purchase price is $12 and we exit at +$22 or more. (without dividend and buyback adjustment)

Our margin of safety is solid, and share buybacks enable us to maintain the price and generate value that will be unlocked over the next 2 years.

We can also value the company on its tangible book value of approximately $30 (CAD). If we think we will exit at a value close to 80% (10-years avg) of the tangible book value. This gives us a very good IRR (+40%) over 2 years.

-Max

Your write up following the last quarter reporting was prescient - as to your concern about the 10 year yields - well spotted back in November. The longer yields have risen, despite short term declines - so - near term improvement in the leveraged REITs has been muted. Prevailing interest rates for TNT appear to have been flat around 4.0% - so expected declines, and current stubbornness of decline - seem to have a limited impact to TNT.

The 'advantageous' purchases have not helped the per unit returns as the absolute earnings have reduced, and management has blamed this on the reduced number of properties - fair enough - but there has been no realized benefit to the reduced units outstanding - other than should some realization event occur - which does not help unit holders.

Hopefully, the dogs are being sold, and remaining properties are better quality with stronger tenants, and lease values.

Hopefully the vacant Calgary property is now sold, which leaves one other vacant property and one low occupancy property - two dogs remaining?

Your comments reflect the improved financial and operating environment, and prospects for the REIT, so why have unit prices dropped, significantly, and continuously? Now approaching the low price range last year when distributions had been discontinued with limited prospects for return to distributions.

Since your research presentation of November - unit prices are down 15%. As you state, at the time of the last quarter report, management told unit holders to wait, another quarter.

Since your previous 3 rd quarter reporting, another quarter has passed = another $9M of cash retention from operations, beyond what has been reported. Since suspension of distributions, cash retention (roughly) 5 quarters x $9M/quarter + $19M equity from property realizations (reported) = $64M, less 'advantageous' purchases of $13, so net cash improvement (repayment of credit line) by ~ $50M or $3/unit, yet stock is down 15% from your report. Why?

Small cap, management controls the REIT, management pays itself significant compensation, management (investor relations??) ignore REIT unit holders communications, management provides no guidance to unit holders looking for cash returns, Canadian listing (??!!), you are right = value trap.

You are correct, REIT legislation and tax rules require distributions (beyond what management describes as 'implied distributions'. You will have seen the magnitude of audit and tax bills - so management has better information than you or I. Management continues to ignore unit holder interest for cash returns - capitulation occurs as unit prices drop = better 'advantageous purchases for benefit of management interests - not unit holders!

In my opinion, it really comes down to management's parameters concerning cash distributions to unit holders - and they are not forthcoming with that information - like yourself, they have not responded to my requests for information - why not? Why would they? Unit holder interests conflict with that of management, so there is no benefit to management for improved market for the units - they control the market.

Your analysis is all correct - the unknown is whether management will comply with REIT requirements for distributions, or at least provide guidance to unit holders as to distribution of their entitlement to cash distributions. Any ideas as to information in that regard?

I hope that TNT works out better than the US REITs have performed with the TNT management team!! I am cutting my losses on those bad investments. And may exit the trap with TNT.

Regards,

DG Hunter

Your insightful, and learned comments are valuable.

I did not suggest that True North, or their management, have a bad reputation, but they may - I don't know and I am not making that assertion. What is problematic to me is the magnitude of, very large, cash fees paid to a management through a related company, with common ownership. There is a conflict of interests between the unit holders, who's cash distributions have been withheld by management, and the management which continues to receive large cash fees paid to, itself. One loses, one gains.

Management is not remitting cash to its unit holders, but does pay, large management fees, to itself. The pain is being felt by the unit holders, not management.

As management has a large ownership interest, with defacto control, the point could be made that absence of distributions is aligned with unit holders. But this is false due to the magnitude of funds/cash flow, in the form of fees extracted and paid as cash to management.

With a small market company, such as this, and in the Canadian stock market, this is always an issue that management bleeds small companies dry, and many go broke - and old story. Although I am not saying that is the case here, but it is the RISK!

Something that does not look right. With all the advantageous share purchases, and associated cancellation of units - the return to the unit holders AFFO/FFO has not increased, (as mathematically it should so all the benefit of expenditure of share buy backs ~$13 management has spent has accomplished nothing on an AFFO/FFO per unit return basis. As always, management will have an explanation for this - which is incorrigible.

Further to the point on per unit holder returns, what happened to the proceeds of the 4 properties sold, that created about $20 net to unit holders. Cash balance is the same - mortgages payable and the line of credit has been paid down - but cash position unchanged = no funds for unitholders.. With debt paid down the and funds avaialble to unit holders, unchanged, and the reported AFFO/FFO to unit holders is unchanged , or dropped- the math does not make sense and does not work.

Should the conditional sale be closed, what will happen to the $10 of equity?

Further, there are another two remaining Toronto properties for sale, strong markets, unsold, although one has no tenants - and that may gut the value of the property, I don't know.

The units are down close to 40% from recent highs, and approaching lows for the year. The fund continues to buy the units, but at a reduced scale,and managment has scaled back insider purchasers. The most informed owner, Management, is personally buying less and directing the fund to be less aggressive. That party has ALL the answers, and the directive is less aggressive buying - why?

There has been no reporting to shareholders as to a plan to return funds to unit holders. They don't answer my calls. And that is a bad sign. They have a investor relations contact - but I have received not response.- why would they bother.

The fact is the managment team has a conflict over payments made to themselves, and not paid to unit holders, yet using those unit holder moneys to repurchase units, and enhance the value of the REIT - which managment controls.

Notwithstanding the outline above, all your points are valid and useful, in the event that management has been fully, and fairly disclosing the affairs of the company, and intentions of management -- which I have not seen or heard,

Is management doing the right thing for the unit holders that bought this REIT for distributions - not received, in over a year., and no suggestion of the prospects of payment until March 2025.?

Managemet has not addressed the above issues with unit holders, and have not addressed the inherent and extreme conflicts between unit holders and management, who are precluding payment to unit holders in lieu of themselves.

Your hypothesis seems to be that with the earnings generated accumulated and unremitted distributions + equity proceeds from property dispositions, represent a signficant amount of funds that could be repatriated to unit holders - but management has not provided a prospect or basis for such an action - but has so far declined the suggestion.

Whether they have to make a 'distribution in cash this year to avoid taxes' - that is a bold statement. Do the buybacks constitute distributions, hence no distributions required. Or are there amortizations/tax losses and such (Revenue Canada) or other tax tricks - tax losses created - to avoid a taxable situation and defer distributions. Look at how much they pay their tax, and audit advisors, to get around such issues.

Meanwhile, large management fees are paid and are current, units are being redeemed,. unit prices are dropping as there is no liquidity as there is no indication of improved prospects for the REIT - management seems to be conducting all affairs for their benefit, in conflict to unit holder interests.

No distribution to unit holders, no foreseeable distributions to unit holders, no commentary from management, management vested interests to freeze out unit holders to capitulation, all works in favour of management. This is an often repeated practice of small cap listed Canadian companies on Canadian exchanges.

Again, if you can indicate how they must change strategy, I would like to know.

Regards,

DGHunter